MIFID INSIGHTS

MiFID II INTC Aggregated Client Account Reporting

Author:

Sophia Fulugunya

Author:

Sophia Fulugunya

Director of Transaction Reporting

21 November 2023

INTC is the MiFID II convention used to report aggregated client orders without implying principal trading. This guide explains how INTC works, common reporting errors, regulator expectations, and practical controls to validate allocations and reconciliations.

Transaction reporting compliance remains a paramount concern for investment firms due to MiFID II's introduction of several changes. Among these, the concept of Aggregated Client Accounts (INTC) has garnered significant attention, posing challenges for many firms. In this article, we'll explore the definition of INTC, its importance, and how Qomply supports investment firms in ensuring compliance.

What is INTC?

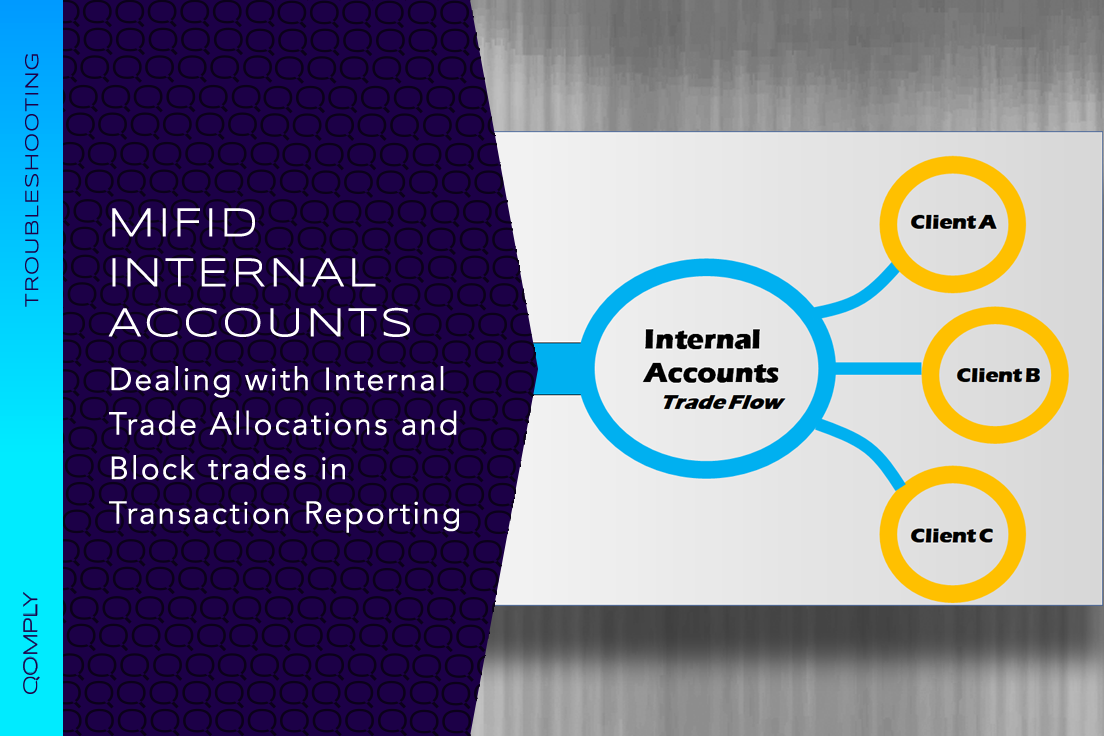

INTC, or Aggregated Client Account, comes into play when investment firms operating in an agency capacity execute orders involving multiple client allocations. INTC allows for the proper reporting of aggregated orders without giving the impression that the firm is dealing in principal. Typically, when executing transactions for a single client, a single report reflects both the market and client sides. However, the aggregation of orders divides these reports into two parts:

Market Side: These reports provide insight into the transaction from the market's perspective, detailing its execution with the market counterparty.

Client Allocations: These reports break down the aggregated orders into individual client allocations, specifying how the orders were distributed among different clients.

To ensure compliance with MiFID II transaction reporting guidelines when utilising INTC, it is crucial to adhere to two key rules:

Balance Equality: At the end of the day, the quantities on the market and client sides must match. In other words, there should be no remaining balance in the INTC. If 50 units were input into INTC, 50 units must be withdrawn.

Multiple clients: INTC should be used exclusively for aggregated client orders and not for single clients.

Additionally, in accordance with the guidelines, firms must report the earliest trade date and time for all client allocations when the market side of the transaction was executed in multiple fills.

Looking forward, ESMA has recognised that it can be difficult to identify which market trades match to which allocations as there is no explicit linkage between the two, other than the ISIN and trade date time. As such, it has proposed the use of a unique code in the buyer/seller fields instead of INTC. If ESMA introduces this change, although it addresses the issue, it would mean that firms would need to change their systems to generate a unique code and insert this into the relevant buyer/seller fields of the market and allocation trades.

How Can Qomply Assist?

Qomply is dedicated to helping investment firms navigate the complexities of MiFID II and ensure adherence to the guidelines concerning INTC. We offer a unique solution that includes rules to verify and validate transactions, checking for any inconsistencies related to the use of INTC. Our experience has shown that investment firms still grapple with the intricacies of INTC, making the need for a reliable and comprehensive solution even more critical.

As an example, we have observed instances where firms are reporting the same LEI in multiple "allocation" reports for the same market side transactions. This is especially an issue where a firm has several sub funds under one LEI. To assist firms in reviewing the reporting for this scenario, our tool highlights any such instances and presents it as a warning.

By leveraging Qomply ReportAssure, investment firms can effectively:

Mitigate Compliance Risks: Our solution helps identify and rectify any non-compliance issues related to the use of INTC, reducing the risk of regulatory penalties and fines.

Streamline Reporting: Qomply Assure streamlines the transaction reporting process, making it more efficient and accurate, ensuring that aggregated client orders are handled correctly.

Improve Operational Efficiency: By automating compliance checks, investment firms can focus on their core operations and reduce the administrative burden of regulatory compliance.

In Conclusion

MiFID II transaction reporting guidelines, especially those related to INTC, are a crucial aspect of regulatory compliance for investment firms. Ensuring the proper use of INTC is essential to avoid regulatory pitfalls. Qomply stands ready to assist investment firms in navigating the complexities of MiFID II and INTC, ensuring that your transactions are reported accurately and in compliance with the latest regulations.

About Qomply

Qomply takes away the pain by getting transaction reporting right the first time.

Qomply’s technology automatically executes a sophisticated matrix of rules and scenarios across reports from field-level to business-logic level. With thousands of validation rules, Qomply easily exceeds the 250 validation rules set forth by the regulators.

Firms are empowered to conduct real-time checks as well as retrospective checks – making Quality Assurance, Remediation Exercises and Day-to-Day reporting straightforward.

Qomply’s easy-to-use dashboard empowers firms to send their reports directly to the regulator – bypassing costly fees with efficient, straight-through processing power.

This all leads to the fewest number of steps in the pipeline of reporting and ensuring reports are right the first time.

For more information, please contact Qomply, on +44 (0) 20 8242 4789 or info@qomply.co.uk

Follow Qomply on social media on Twitter (https://twitter.com/QomplyRegTools) and LinkedIn (https://www.linkedin.com/company/qomply/)

Free Events, Tools and Information Directly to Your Inbox